The current escalation in the Middle East (March 2026) has moved beyond regional skirmishes into a full-scale disruption of some of the world’s most critical trade veins. For Indian exporters, the “West Asia problem” is no longer a distant geopolitical risk — it’s a daily line item on their balance sheets.

With the Strait of Hormuz on edge and Red Sea routes reverting to “emergency mode”, Indian supply chains are being forced into expensive detours, tougher contract negotiations, and continuous risk re-pricing.

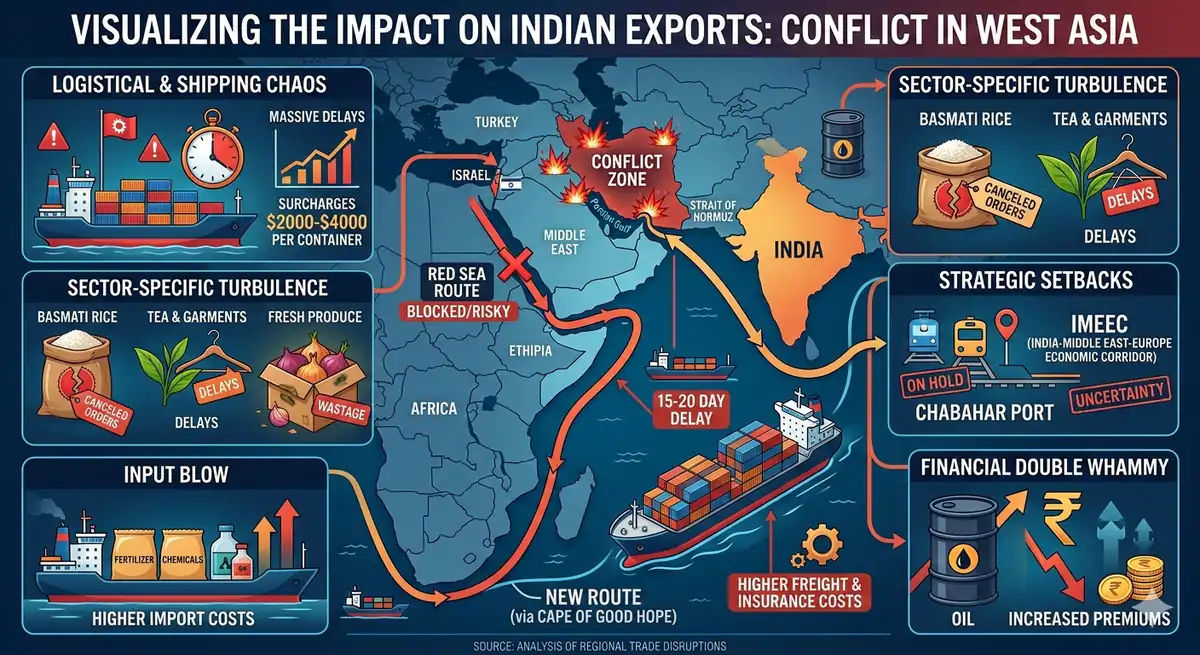

1. The Logistical “Cape” Trap

As the conflict intensifies, shipping majors have once again hit the “reroute” button. To avoid the Red Sea and an increasingly volatile Gulf, container lines are steering vessels around the Cape of Good Hope instead of through Suez-linked corridors.

- The Detour: Vessels bound for Europe and the US East Coast are adding 15–20 days to standard sailing times.

- The Penalty: Extra steaming days mean higher bunker consumption, crew costs, and opportunity loss on vessel rotations.

- The Cost: “Emergency Conflict Surcharges” in the range of $2,000–$4,000 per container are becoming common on key lanes.

For an Indian exporter on thin margins, this is not just a logistics footnote — it is the difference between a profitable shipment and a loss-making one.

2. Sector-Specific Turbulence

While every exporter is feeling the squeeze, some sectors are in the direct line of fire:

Basmati Rice & Tea

Iran and the broader Gulf region together account for nearly 50% of India’s Basmati exports. With the Strait of Hormuz under threat, industry bodies are advising a shift from CIF to FOB contracts, pushing insurance and freight risk back onto the buyer.

Textiles & Garments

Fashion is time-sensitive. A 20-day delay via the Cape can mean “Summer Collections” landing in autumn, triggering order cancellations, markdowns, and damaged brand relationships for Indian suppliers.

Onions & Fresh Produce

West Asia absorbs around 15% of India’s onion exports. With ports operating at limited capacity and vessel calls becoming irregular, perishable consignments are literally rotting at the docks.

3. The Hidden “Input” Blow

The trade shock is not just about what leaves Indian shores — it is equally about what comes in to power future exports.

- Fertilizer squeeze: India imports a large share of its sulphur (critical for DAP/SSP fertilizers) from Qatar, UAE, and Oman. If these cargoes are delayed ahead of the Kharif season, the yield impact will show up in exportable surplus 6–12 months down the line.

- Chemical intermediates: Rising “landed cost” on imported inputs is compressing already tight margins for chemical and specialty manufacturers who compete on cents per kilo in global markets.

In other words, today’s freight and input disruption can quietly become tomorrow’s volume and competitiveness problem.

4. Strategic Setbacks: IMEEC and Chabahar

Beyond month-to-month freight bills, the conflict is also freezing long-term connectivity bets:

- IMEEC “on ice”: The India-Middle East-Europe Economic Corridor (IMEEC), designed as India’s answer to the new Silk Road, hinges on stable nodes such as the Israeli port of Haifa — now sitting in the middle of an active conflict theatre.

- Chabahar uncertainty: The Chabahar Port in Iran, India’s strategic gateway into Central Asia and Afghanistan, faces renewed uncertainty as sanctions risk and regional instability rise again.

For Indian exporters and logistics planners, this means corridor diversification plans must be revisited — with more conservative timelines and more expensive risk buffers.

5. The Financial “Double Whammy”

Every spike in crude prices hits India twice — first through the national import bill, and then through exporter cost structures.

- Macro hit: For every $1 increase in crude, India’s annual import bill swells by roughly $2 billion, pressuring the Rupee and foreign exchange reserves.

- Exporter dilemma: A weaker Rupee looks positive for exporters on paper, but when combined with 30–50% higher freight and insurance premiums, the notional FX benefit is quickly eaten away.

Indian exporters are being forced to choose between absorbing massive logistics costs or pricing themselves out of an already cautious global demand environment.

Where Do Indian Exporters Go from Here?

“Resilience” has become the word of the year for Indian trade — but resilience is not free. It demands smarter contracts, diversified routes, and better risk-sharing mechanisms with buyers.

Without calibrated policy support — from targeted freight assistance and export credit backstops to clearer insurance frameworks for conflict zones — India’s export growth targets for 2026 start to look like a steep uphill climb rather than a glide path.

For buyers and partners across the world, understanding these pressures is key to structuring sustainable, long-term relationships with Indian suppliers in a more volatile decade for global trade.

Talk to Mukta Exports About Supply Chain Resilience

If you are re-evaluating sourcing strategies out of India in light of the Iran-Israel conflict and Red Sea disruptions, our team can help you model landed costs, build contingency plans, and secure reliable spice supply.

Let’s de-risk your spice and agri-commodity supply chain

Reach out for a discussion on routes, timelines, and contract structures tailored to your markets.

Contact Us